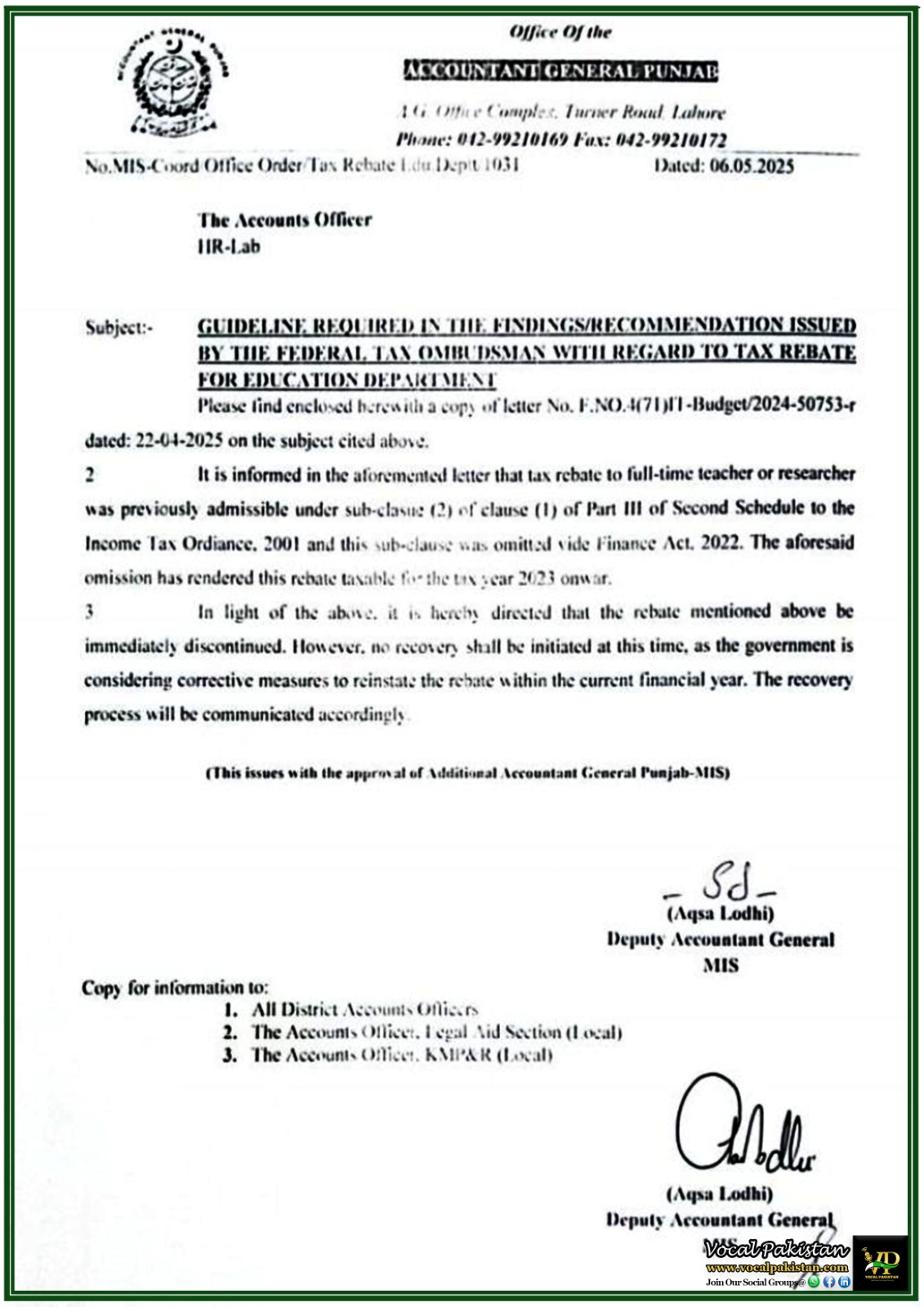

Notification / OM No.

F.No. 2(2)BR-II/2008-590

Dated:

09-March-2009

Notification Issued By:

FINANCE DIVISION (Budget Wing) GOVERNMENT OF PAKISTAN

GOVERNMENT OF PAKISTAN

FINANCE DIVISION

(Budget Wing)

F.No. 2(2)BR-II/2008-590

Islamabad, March 09, 2009

OFFICE MEMORANDUM

Subject: REVISED PROCEDURE FOR OPERATION OF LAPSABLE ASSIGNMENT ACCOUNTS FOR FEDERAL GOVERNMENT

The undersigned is directed to refer Finance Division letter No. F. 2(2) BR-II/2008-551 dated 03rd March, 2009 on the above subject.

2. In this regards the minutes of the meeting is enclosed for information and necessary action.

Deputy Secretary (BR-II)

MINUTES OF THE MEETING HELD ON 5TH MARCH, 2009 UNDER THE CHAIRMANSHIP OF THE ADVISER TO THE PRIME MINISTER ON FINANCE AND REVENUE

Subject: Revised Procedure for Operation of Lapsable Assignment Accounts of Federal Government.

A meeting was held on 5th March, 2009 under the Chairmanship of Adviser to the Prime Minister on Finance and Revenue to discuss the issue relating to implementation of Lapsable Assignment Account procedure with reference to PWP-I & II. Ms. Hina Rabbani Khar, Minister of State for Finance was also present. The list of participants is attached at Annex-I. The following decisions were taken:-

- It was agreed in the meeting that the funds for PWP-I & II would be utilized through Lapsable Assignment Account already opened by the SNGPL and SSGCL.

- Companies may continue procurement of material in accordance with their existing procedure. The cheques equivalent to the material issued on development work relating to government share of these expenses may be drawn from the Lapsable Assignment Account in favour of Company’s Account on need basis.

- It was also agreed that Companies may continue payments to its supplier in accordance with their existing procedure. Withdrawal from Lapsable Assignment Account may be made to the extent of the GOP share of expenditure for credit to Company’s Account.

- The amount not actually drawn against the authorized ceiling at the close of the year if otherwise committed and certified as such by the executing agencies would be renewed for drawal/disbursement during the subsequent year through budgetary allocation. The funds would be released in the Lapsable Assignment Account in the first month of the next Financial Year without waiting for the instruction for the operations of the Budget for that specific year on a formal report/request from the Companies.

- Companies may charge certain percentage of the total material cost and withdrawal of such amount from Lapsable Assignment Account on monthly basis subject to the condition that such percentage would be in accordance with the existing practices.

- The audit of expenditure incurred in connection with schemes of PWP-I & II will be done on annual basis by Auditor General of Pakistan as per existing practice

- It was also agreed that instead of two main Lapsable Assignment Accounts of PEPCO under PWP-I and PWP-II, separate Lapsable Assignment Accounts under PWP-I & PWP-II would be opened for each DISCO, under intimation to PEPCO for coordination and monitoring. Operation of these Lapsable Assignment Accounts shall be subject to the above-mentioned guidelines.

Stay updated for further details and clarifications regarding the above mentioned or any other notification, please do not hesitate to reach out to our Facebook Group.